I’m curious if anybody with more insight than me (i.e. any whatsoever) has any predictions on how the low price of oil will effect fracking in the Bakken oil field? My understanding is that fracking is a more cost intensive form of extraction and they could be the first to shut down.

Do you think oil production in ND is going to slow down as a result of the price drop? Are the days of $100 a barrel over?

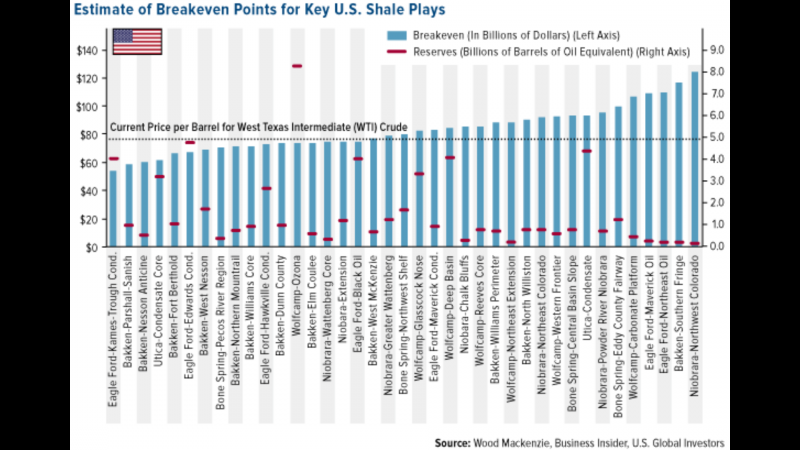

Wow…that’s awesome. Thanks for posting. I didn’t realize there was such a disparity between costs of extraction just within Bakken. What would cause the breakeven for Parshall Sanish to be half of the Bakken Southern Fringe? Wouldn’t they both be extracted with fracking?

^ It’s due to differences in per well EURs and well drilling costs. Plays like the Bakken, Eagle Ford, Marcellus are far from homogeneous, so well performance varies significantly across the plays. That’s why Wood Mackenzie (the firm that made that chart) breaks the plays into “sub-plays”.

As somebody who spends pretty much all of their work week looking at unconventional oil and gas, the lower oil prices won’t have a huge impact. The companies that are drilling most of the wells are independents, and they want production growth. They’re not going to engage in value destructive drilling (most of the time, though they may do that to hold leases) but if due to oil prices the IRR of a well is now 25% at $80 oil vs. 50% at $100 oil (making numbers up here as I don’t have my work laptop), they’re still making money drilling new wells. They just might drill fewer wells now vs. 6 months ago.

Kanuck, you’re getting 25% IRR’s from the Bakken at $76/bbl (in USD)? I see only ~15% IRR at current pricing on 600Mboe EUR, 8.5 million well cost (which I view as about average for core Bakken acreage). Some companies have lower operating cost structures (CLR), but all of these independents get $7-8/bbl less than WTI for their oil getting it to market. I don’t see the 450mboe EUR wells economic at current pricing, but those are less attractive acreage positions in the Bakken.

Agree companies will still drill pretty aggressively, but I think they’ve got to cut back on their capex. I think keeping capex at 2014 levels is not prudent capital management.

A good deal of the economics on these wells comes down to (a) well costs and (b) proprietary drilling techniques of the individual companies; some of which are a materially better than others.

Read what I put in parenthesis… I said I was just making up numbers to illustrate a point that some companies are still making money, albeit less. If I were at work I could some more accurate figures.

^ My mistake. You seem to be a knowledgable guy based on what I’ve read on this stuff, so I didn’t think you’d mention numbers if they didn’t have merit, even if it’s just off the top of your head #'s. No worries.

Only if you believe this pricing to be a long term trend. You’ll start to see well costs and servicing prices come down at these price levels, and firms that take advantage of that (along with acquiring prospects at lower prices) will be best positioned for recovery. This is typical of the analyst mindset though and what drives value destruction. The street wants companies to be aggressively spending during booms and cutting back during tougher times. The most successful companies are those that stay the course and manage their business on a longer term cycle. There is great buying opportunity today. Now if you believe oil is going to $60, fine, but then you should just stop following the industry as it offers no investment opportunity at that level.

Not every well has the same cost and expected recoveries. You can’t look at the average break even and assume no well will be profitable below that level. Its an average.

I think companies, as a whole, have been too aggressive spending in prior years – nobody but EOG actually produces free cash flow. Full disclosure, I don’t particularly like these U.S.-based unconventional producers, with the exception of EOG and some of the top Marcellus acreage holders (RRC, COG, EQT), mainly b/c I don’t like the cash flow profiles of these high decline-rate wells with very high capital intensity (heavy reliance on debt). I prefer the Canadian oil sands guys long-term.

If you’re a Bakken producer and only getting a 15% IRR on what you hope to be a 600 MBoe EUR well, I hope you’ll think twice about some of your lesser acreage positions with WTI at $75/bbl. However, someone with primo acreage and a low cost structure, like Continental Resources, I’m cool with them still investing (in the Bakken) b/c they should still be getting +20% returns by my estimates.

I appreciate your thoughts, geo, b/c you know what you’re talking about, but IMO the E&P industry has been heavily reliant upon debt capital in recent years to bridge these large funding gaps. Unless you’re able to generate free cash flow to support your capex (EOG is the only one I’m aware of that does), I think companies have to cut back. Keeping investment in new wells up at 2014 levels next year is borderline reckless for many b/c financial leverage will really increase, as operational cash flows are now going to be lower with crude prices dropping 25%, so you’ll rely even more on debt financing which could eventually be quite destructive. Too risky for my liking, but I have a negative bias toward this type of production.

The only oil company that I actually listened to their reporting first hand is HK and they are cutting their rig count in half for 2015, 12 to 6. Are they an anomaly? Seems the prevailing narrative is that there won’t be much of a slow down? How could that possibly be? The risk/return is certainly much different at 75. These aren’t offshore projects with five year lead times.

They are a bit of an anomaly slowing down that much, but they have to. They don’t have the money and don’t have the cash flow to support their capex. Not to mention $3.5B in debt, most of it at 9-10%. So call it $300M a year in interest and their revenue this year ought to be ~$1.1-1.2B. Every metric scares me. Their 2014 capex budget was about $1B. Unsustainable.

As an aside, I don’t really like HK as a company. Their management is arrogant and cocky and assumes they can just “do it again” like Petrohawk, but they’ve struck out in basically every play they’ve tried this time around. Most of their Bakken stuff is 2nd/3rd tier, though they’re developing the smaller part that is decent.

Looks like they have some decent hedges on. At least their arrogance didn’t stop them from buying protection or cutting back . They can handle at least a couple years of pain. There must be a price where they would make sense as an option…two dollars? One dollar?

Can anyone comment on what the typical (yeah oxy-moron) financing structure is like for these projects i.e. recourse/non-recourse, gearing/leverage, financial covenants, term structure. ect?

^ If I thought anybody wanted to buy HK, I might consider it a speculative buy right now. But…I just don’t see them as an attractive acquisition target at an EV of ~$4.8B (1.3B mkt cap plus debt). My company’s valuation of HK is considerably lower than that, mainly because their asset portfolio is a mashup of 2nd tier assets that would be non-core to most anybody else and because of that, probably not worth paying enough of a premium for the equity to get a lot of upside on a buyout offer. As far as takeover targets go, there are better options out there.

Don’t get me wrong, there is probably money to be made/lost trading HK b/c its so volatile, but that’s it, IMO.

I’ve reviewed several of these type of deals and it seems to vary based on the financial strength of the company or principles. However, non-recourse notes are exceedingly rare after the chaos they cause in the last oil crash. But they have been reappearing as of late.

Also, financing is often not based on spot rates. When the spot prices were 110, there were still some calculating the financial ratios at a spot of 75.