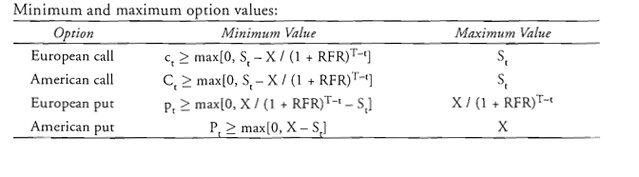

Can anyone help me explain this, I have been confused much: American type- Minimum Value: -Why in Put option, we dont take into account TIME VALUE but do so in American Call? Maximum value: -Why only in case of European put we take into account of time value ( max = X/(1+RFR)^t ), in all other cases we dont ( Max value are Stock price or strike price). Please see the link here: http://farm3.static.flickr.com/2625/5714131285_31d3d416c0_z.jpg I have had difficultites in trying to memorize these values since I cannot understand the rationale behind it. Any tips?

{kind=link}

American put/call options can be exercised at any time, so by that logic, you shouldn’t need to take into account time value on either. However, that would mean that the minimum value of an American call would actually be lower than the minimum value for a European call – which makes no sense because an American call (which can be exercised anytime) is obviously not going to be worth less than a European call (which can only be exercised at maturity). Hence, we adjust the minimum value of the American call upwards by taking time value into account. (ie using the same formula as for European calls.)

Great explanation Kia!

cheers  gotta admit I’m a bit confused on the maximum values for call options being the stock price though…when i read it in the textbook I just accepted that it was right, but now I’m finding it hard to explain why. eg let’s say a stock is trading at $100 and you’re looking to buy a call option with an exercise price of $50. Why is the maximum value of the call option $100 – ie why would you pay $100 for the right to buy the stock for $50, a total spend of $150, instead of just buying the stock. anyone?

gotta admit I’m a bit confused on the maximum values for call options being the stock price though…when i read it in the textbook I just accepted that it was right, but now I’m finding it hard to explain why. eg let’s say a stock is trading at $100 and you’re looking to buy a call option with an exercise price of $50. Why is the maximum value of the call option $100 – ie why would you pay $100 for the right to buy the stock for $50, a total spend of $150, instead of just buying the stock. anyone?

Its the max possible value for a call, which requires the minimum possible exercise price (0). in this case the max you would pay for the call would be the stock price. To answer the your example, you might pay $100 for the right to buy the stock for $50 if there is a looong time to expiration (high time value). In no circumstance however would you pay more than the stock price, $100. Hope that helps man!

Kiakaha Wrote: ------------------------------------------------------- > cheers gotta admit I’m a bit confused on the > maximum values for call options being the stock > price though…when i read it in the textbook I > just accepted that it was right, but now I’m > finding it hard to explain why. > > eg let’s say a stock is trading at $100 and you’re > looking to buy a call option with an exercise > price of $50. Why is the maximum value of the call > option $100 – ie why would you pay $100 for the > right to buy the stock for $50, a total spend of > $150, instead of just buying the stock. > > anyone? Kia, From my understanding, this value is the intrisic value of the option, not the option Premium- the actual cash you spend on the option. To compute option’s premium we use Black scholes, as some of you may know . THat is quite complicated calculation and require several inputs i.e volatilty…Again, this is the instrinsic value ( which plus time value = total value of the option) Hope this helps.

Here is the link for definition: http://www.investopedia.com/terms/i/intrinsicvalue.asp 1. For example, value investors that follow fundamental analysis look at both qualitative (business model, governance, target market factors etc.) and quantitative (ratios, financial statement analysis, etc.) aspects of a business to see if the business is currently out of favor with the market and is really worth much more than its current valuation. 2. Intrinsic value in options is the in-the-money portion of the option’s premium. For example, If a call options strike price is $15 and the underlying stock’s market price is at $25, then the intrinsic value of the call option is $10. An option is usually never worth less than what an option holder can receive if the option is exercised.

JonnyKay, that was great, thanks! Maxmeomeo – you might be right, I don’t know enough about options to tell either way! Not looking forward to black scholes when we get past level 1

“you might pay $100 for the right to buy the stock for $50 if there is a looong time to expiration (high time value).” Not so. You would pay $100 to buy the stock for $50 tomorrow if the stock was trading at > $150. "To compute option’s premium we use Black scholes, as some of you may know " Not so. The options premium is determined in the market by the usual market process. Black Scholes can then transform the price/strike into implied volatility/delta which is in some ways a more sensible way to talk about options (e.g., “a 25 delta call is trading at 30 vol” is probably still true if the price of the underlier moves but “a 50 call is trading at 4” isn’t true if the underlier moves). The implied vol in BS isn’t something that can be calculated and is surely not historic vol.

Ok I am not arguing your point. What I am trying to say here is they are mistaken between INTRINSIC VALUE of option and PREMIUM ( or the cost) of option. They are totally different definitions!

JoeyDVivre Wrote: ------------------------------------------------------- > “you might pay $100 for the right to buy the stock > for $50 if there is a looong time to expiration > (high time value).” > > Not so. You would pay $100 to buy the stock for > $50 tomorrow if the stock was trading at > $150. > Kia’s example assumes that the stock is trading for 50. Jonny’s explanation is correct.

The first question about American call and put option can be answered by an assumption about the stock: no dividend. If we construct two portfolios, one is C+K*e^(-rt), another one is P+S0. Their future values at time t all equal Max(St, K). As there is no income for a stock, so it’s impossible to get a perfect time to execute an American call option and you still need to consider the time value of your cash position in the first portfolio. But when you consider the second portfolio, you won’t have a position in cash and you don’t need to adjust the time value.

As for the second question, we always assume So > Present Value of K when pricing a call option otherwise, the call option is useless and has no value. Thus, if the value of call option either European or American is higher than So at the spot market, we will buy the stock directly and not enter into a position in the call, which sets the maximum value of a call. When it comes to the put, we assume PV of future K > So under some logic. thus the maximum value of put should focus on the PV of K. However, there will be a difference between the time value of K for European and American puts.

Hope it can make a little sense.