I’m wondering if someone could help me out with this…not many bond people around here, I guess, but maybe.

I would like to understand it, when you compare corporate bonds based on relative value, what do you look at? I’m interested especially in discovering credit spread /yield pickup opportunities.

Could anyone recommend a book or sell side research paper which would help me get a grasp, please. I’d be sooo grateful. Thanks a mill!

An economist saw that an apple was $100 and two apples were $200; he therefore concluded that the markets were fairly priced.

IMO, there are a lot of mispricings happening in the bond market because of the hunt for yield. It comes back to carefully analyzing the financials(looking at Cash/marketable securities to total debt, and etc.). It’s back to the basics.

Below are two mispricings tricks I use when bond buying:

BUT if you want to go the credit spread route, I would say look at the bonds right below investment grade; so the BB+/Ba1 level. Many of these bonds, based on the financials and fundamentals are no different than BBB-/Baa3 but pricing can be different enough to present an opportunity(many funds will only hold investment grade bonds). Always siff through financials and go over ratios; there are no shortcuts; it’s back to the basics.

Look at continously callable bonds as they approach their next call date. Because they can only be redeemed at their call price; these bonds prices approach their call price the closre they get to their next call date. The days before it’s announced whether or not the bonds will be called presents a buying opportunity(you will have to do some analysis to determine if these bonds will be called)

Use FINRA Bond Center or another third party site to view unbiased pricing. Some brokers padd the bond price as opposed to charging a flat commission.

P.S…I consider myself a bond person and there aren’t many people like that on here.

The bond market is HUGE. It takes over $2 trillion of credit origination a day to keep the world moving which makes the equity markets look like peanuts. As an investment grade corporate credit analyst, I’m looking at spreads all day long. A company’s credit spreads against peers and against a benchmark – mostly Barclays Indices. This is mainly how I judge relative value. I’m always thinking if there’s enough spread to price the risk, do I think it’s going to tighten/widen, what are the rating agencies doing (ratings drift), where’s the most value in the company’s credit curve - is the curve too flat or too steep. Of course this is based on fundamental analysis at the issuer level and industry level. Interestingly, some of the things that might boost equity prices will make spreads widen out. Example – debt financed buybacks. Luckily, I let the portfolio managers worry about interest rate risk.

@Krisztina, I would send you some sell side credit research but PMing has disappeared. PM me if it comes back and I’ll send you some.

Thanks a lot for your input! The thing is that I’m ok with fundamental credit analysis and I am familiar with corporate bonds, working with both high grade and high yield instruments (only on the credit side, though). However, my job never required me to consider/evaluate them from more of a ‘trading’ prospective, which is silly, and I’d like to venture into the field of RV. I have read an awful lot of books (from Fabozzi, Choudhry, etc) recently about relevant topics but…I feel a little bit left in the dark when I try to figure it out how real analysts do this in the real world (spotting RV opportunities/ generating investment ideas- as they say). I see where you are coming from when you talk about the BB+/BBB- threshold, why it might be beneficious to go for a bond with an upcoming call date attached or the agency problem (wealth transfer to shareholders, unfriendly move towards bondholders), what I don’t quite see is how the quant/technical part of the analysis may look like.

What’s the benchmark based on which you calculate various ‘spreads’ and what are those spreads (YTM, I, Z, OAS, ASW, STW, etc?) you want to look at? Are there any specific measures/spread related ratios you usually check, when you make a bond-to-bond comparison (in the same/ similar rating bucket)? And then of course you may consider trades which involve CDS. I’m not sure if it’s clear what I am curious about, because I am afraid it’s a way too large topic, anyway, I’m awfully grateful for all the comments above.

@spunboy Couldn’t find PM function either, here is an e-mail address.Thank you soooo much for your kind offer, can’t wait!

@Krisztina - I sent a few research reports to the email you posted. It was a big file though so let me if you got it or not. I might need to resend them one at a time.

To answer your question about spreads, I primarily look at OAS or Z-spreads.

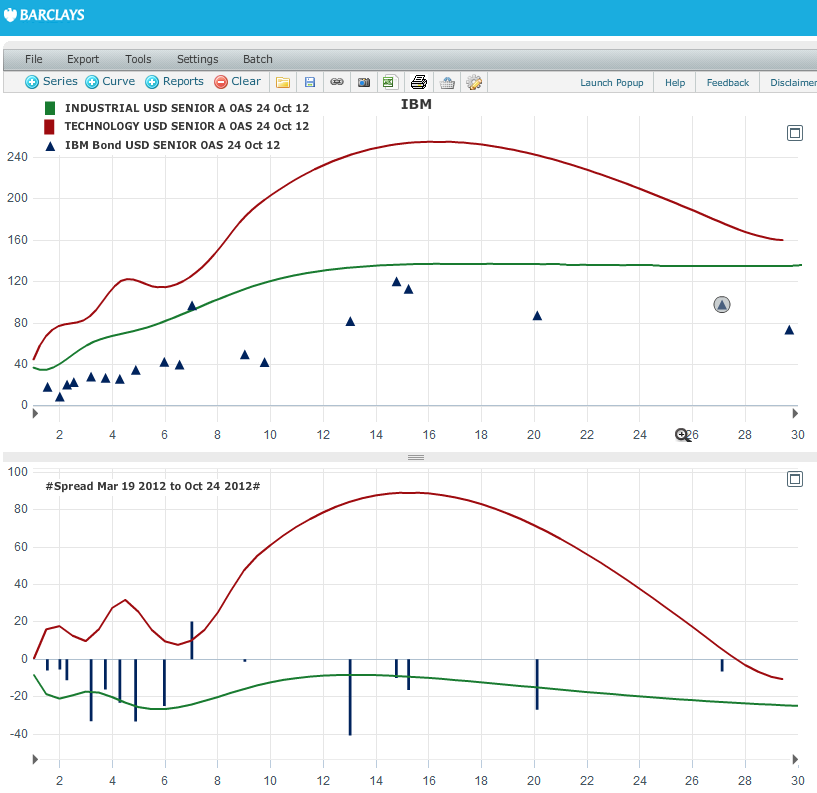

Barclays has an awesome tool that they call CURVE. The screen shot below is IBM’s credit curve – think of it as a yield curve except that the y-axis is the OAS of IBM’s debt. So what this curve is telling you is that IBM trades well through the ‘A’ Rated Tech Index and through the broader ‘A’ Rated Industrial Index.

The lower chart shows you how much the various curves have moved in the set period. Here, IBM’s debt mostly tightened while the ‘A’ Rated Tech Index widened. IBM’s debt also performed better than the broader ‘A’ Rated Industrial Index. In this particular case, the ‘A’ Tech Index underperformed mainly due to HPQ. HPQs spreads have widened a lot in the past couple of months. A better gauge of IBM’s performance would be to look at the ‘A’ Industrial Index.

@spunboy Thanks a lot for your reply, I am in the similar boat as the OP. I find myself struggling as well when it comes to relative value analysis in credit. I was hoping if you could send me those research papers as well. It will be a big help!

Cheers !