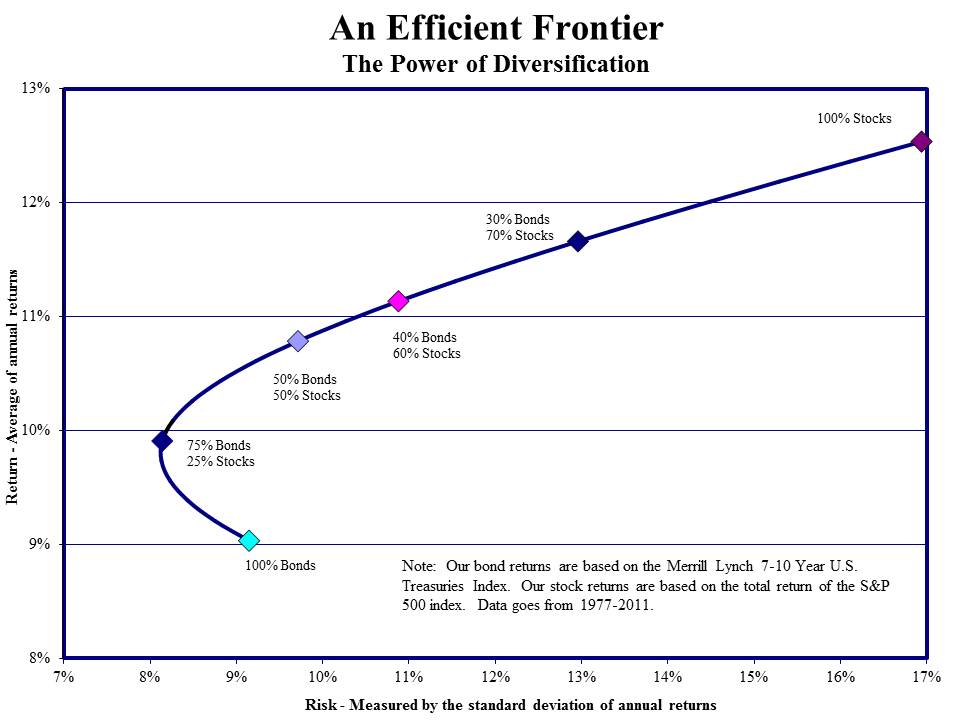

Anyone know why when we we calculate the standard deviation for two corner portfolios we do not have to square the weights and square the standard deviation to solve? I understand that in some cases we consider the correlation between the two portfolios to be 1, so standard deviation is slightly overstated…

…but I am more or less asking why in all other cases we need to square the weights and this case we do not.

If you have done a bit of mathematics, you may know that (a+b)²= a² + b² + 2ab

You may have understood that we consider two adjacent portfolios to be almost perfectly correlated i.e. we assume their coefficient of correlation is 1 (we know in reality that they are less than perfectly positively correlated so our computation will overestimate the standard deviation a bit).

As a result of this assumption, the variance of a portfolio on the efficient frontier between adjacent portfolio 1 (P1) and adjacent portfolio 2 (P2) will be :

w² stddev(P1)² + (1-w)² stddev(P2)² + (1-w) w stddev(P1) stddev(P2)

You will note that, according to the equation given above, this is equal to [w stddev(P1) + (1-w) stddev(P2)] ²

You take the square root of that to go from the variance to the standard deviation and it gives you w stddev(P1) + (1-w) stddev(P2)