I don’t know first-hand that it is, but I’m happy to believe the people here who say that it is.

I will be posting further; I’m just waiting for one more reply.

I don’t know first-hand that it is, but I’m happy to believe the people here who say that it is.

I will be posting further; I’m just waiting for one more reply.

Cool, because I’m really interested in this (for some odd reason).

It’s a long thread, but it was my understanding he did NOT admit delta was an approximation and never heard it was. That’s been long discussed, but I do want to know how much delta varies from in-the-money probabilities under various scenarios.

I’m looking forward to this. Although, they might not give you much, because they could assume you’re trying to poach their software. We will see…

If they simply give me a critique of my approach, that’ll be worth a lot, and won’t tip their hand.

Here’s my take on it.

There are 3 ways you could this.

For (1):

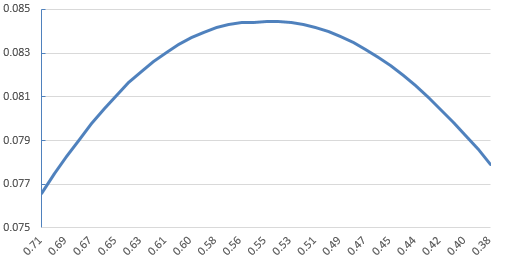

The probability becomes N(d2), by definition, the risk-adjusted probability that the option will be exercised, for each strike price, and hence each delta. Continuing on our previous example of S0=19.36, the expected exercise risk-adjusted probability with respect to delta looks like:

Interesting to note that delta becomes a worse predictor of ITM ending probability as it approaches the bottom of theta θ (or peaks in abs value). Or in other words, it becomes a worse predictor at higher deltas as the time to maturity increases, and ATM (delta = 0.5) just before maturity.

I’ll try to make a post about the other two soon.

Man, this thread turned into way more than I originally expected. Good stuff guys.

I assume whats on the website is nothing fancy. I searched ‘itos lemma excel’ and got this, http://www.realoptions.org/papers1999/WINSTONExcel.PDF

(I’m no good with excel)

They’ve basically used the same method I did, nothing fancy indeed.

At the expense of beating a dead horse, should we just assume Mr. Smart’s estimates of delta versus in-the-money probability are correct? If so, I’ll say delta is a flawed, but handy back-of-the-envelope estimation for probability of exercise.

My guess is that S2000 has yet to hear back from the people he contacted.

increasing in demand call… does it effact in delt or vega if the asset price does not move ?