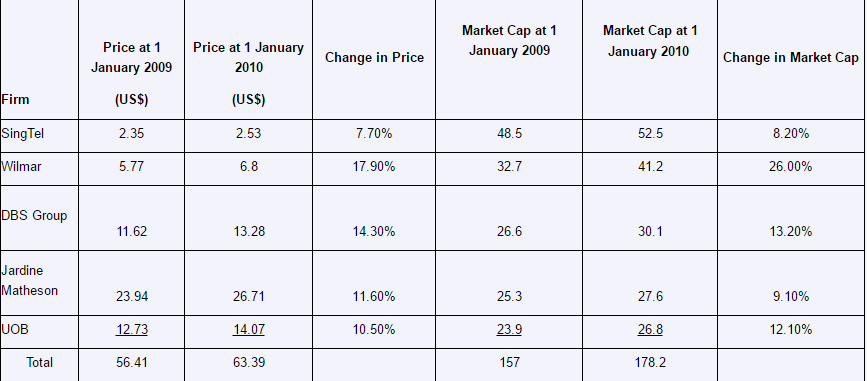

Based on Exhibit 1, for the year 2009, assuming no stock splits or stock dividends for the stock components and no rebalancing, which of these index structures would have most likely resulted in the largest return for the GSI?

I don’t think there is an intuitive answer to this one. You’re going to have to calculate the returns yourself. They give you market-cap in their answer which is 13.5% = (178.2 - 157)/157.

Equal weight would be sum of (change in price * 0.2). (7.7% + 17.90% + 14.30% + 11.60% + 10.50%) * 0.20 = 12.4%

In fact the answer is, in a way, probably discutable.

One important thing is that indexes are not investables.

On an index point of view, the CW resulted in the highstest variation. CFAI ask for the largest index variation and it seems right.

However, from an investor point of view, I guess, total return (with no dividend) point of view, the final result is quite different => assuming the investor portfolio at t=0 waw composed of the stocks according to the various weighting schemes.

Assuming we are searching for the best weighting scheme at t=0 that maximize the index return over 1y.

At t=1 year, index return should be equal to sum(i =1 to 5) wi*Ri where wi is the weight of the stock i and Ri the price return (no dividend) over the year.