Need some clarification on this, not really sure if i’m thinking about this correctly.

If a bond with a coupon or some type of MBS is considered to have negative convexity, that means the bond will till have a positive return (BEY) when interest rates shift up, is that correct?

Once rates increases to a point where total return is negative, is the bond still considered to have negative convexity?

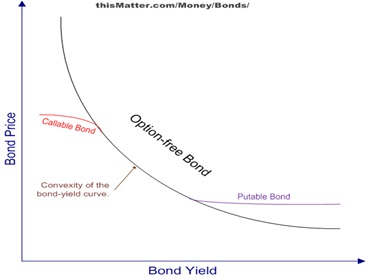

No, I meant that the price is increasing at a decreasing rate. Look at the graph you posted: the red section labeled Callable Bond shows the region of negative convexity. As the YTM decreases, the bond price continues to increase, but more slowly than that of on option-free bond. The price of the option-free bond increases at an increasing rate (it has positive convexity) while the price of the callable bond increases at a decreasing rate (it has negative convexity).

Ah ok, visually that puts things into perspective now. that option of the issuer potentially calling back the bond really can put a damper on things.

so to close the loop. negative convexity is in reference to bonds with callable options. and negative effective duration is in reference to coupon securities like MBS?

Much thanks S2000, expected nothing less from the securitized expert.

For an MBS, as interest rates drop, mortgagees will prepay their principal balances at a very high rate to take advantage of lower interest rates. All these inflows get reinvested at lower rates, so the value of the MBS will suffer in a similar fashion to the callable bond.

MBSs display negative convexity at low interest rates, for the reason that breadmaker just outlined.

Very few securities have negative effective duration. Interest-only (IO) strips can have negative effective duration at low interest rates, which makes them very interesting bonds indeed.

Sorry to bump an old thread but wanted to get some clarification on the following statement from the Schwesser text

“If rates increase, the issuer has no incentive to call and the price declines like a comparable option-free bond. Said another way, the duration and rate of price loss increase as rates increase.”

Based on the graph above, the gradient declines when the rates increase so shouldn’t the rate of price loss decrease?