Hi,

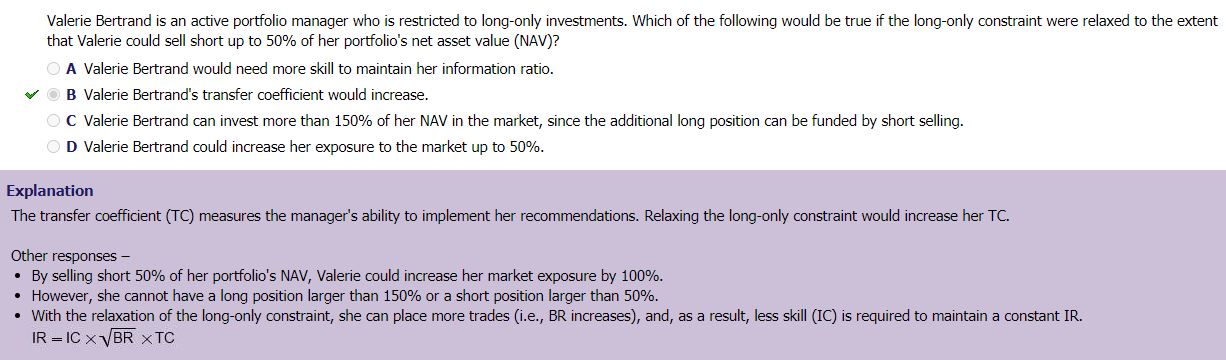

This is from a MC question I had recently (it’s from CAIA but the forum is more active here). See attached image. I don’t understand how this makes sense " By selling short 50% of her portfolio’s NAV, Valerie could increase her market exposure by 100%. However, she cannot have a long position larger than 150% or a short position larger than 50%." Shouldn’t it be 50% increase in market exposure?

Capture|690x202

{kind=link}