Of course, one reason is callable bond as interest rate goes down, the price flattens out but what’s the second reason?

you mean, negative convexity can occur?

Right, sorry that’s what I meant.

mortgage?

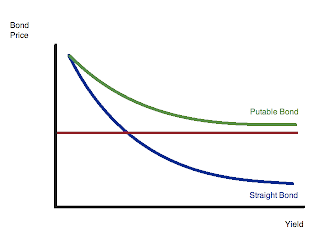

Less convexity when Interest goes up for Putable Bonds… http://2.bp.blogspot.com/_RUe4EZEDFco/ShMC8OxM7LI/AAAAAAAAAqU/P6_xugHA8VQ/s320/Putable+Bond.png

{kind=link}

I would say MBS is the 2nd one, like pupdawg82

Yes, in case where they would exhibit Negative Convexity…

MBS and callable bonds are examples of securities that exhibit negative convexity. I meant to ask whether there is another way that a security can have negative convexity except when the interest rate goes down.