There’s something new everyday. Stumped for a good 10 minutes to say the least, then I gave up.

There’s something new everyday. Stumped for a good 10 minutes to say the least, then I gave up.

B? I got 0.6233

They want you to use COV(A,B) = Ba*Bb*systematic variance

VAR(A) = (Ba^2) *Systematic Variance + idiosyncratic variance of a

VAR(B) = (Bb^2) *Systematic Variance + idiosyncratic variance of b

COV(A,B) / ([VAR(A)*VAR(B)]^0.5) = CORR(A,B)

If you use the market model (and understand the math a bit) you don’t need to remember this formula as you can derive it. Take the variance of Ri which is VAR( alphai + Bi*Rm + ei) = (Bi^2) * Var(Rm) + Var(ei) … do the same for the covariance of the two returns and it will give you the pieces to the puzzle.

Market Model section (unadjusted historical beta)

corr (a,b) = beta(a) * beta (b) * var(market)

So : corr = 0,6 * 1,5 * 0,04 = 0,036

Thats Covariance… then you have to go from that to Correlation.

You found the covariance, sir.

Edit: I should review my market model formulas

PM is a killer… can get you with 2 item sets

I say B.

Tickersu is right

i think its B… you find corr = .036… you use the formula r=(cov)/StdDev(a)*StdDev(b) … solve for std dev for both a and b… square root of (b^2* var market + var unsystematic) … fill that into the corr formula and you get something close to .036/.058

You guys are right, i wrote down the formula for covariance.

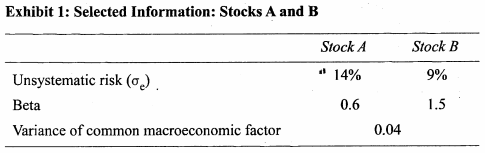

You have the unsystematic risks so you can calculate :

Var (a) = beta(a)^2 * var(market) + var(e-a)

Var (b) = beta(b)^2 * var(market) + var(e-b)

At the same time : Cov (a,b) = corr (a,b) * sqrt [var (a) * var (b)]

All in all :

Covar = 1,5*0,6*0,04 = 0,036

Var a = 0,6^2*0,04 + 0,14^2 = 0,034

Var b = 1,5^2*0,04 + 0,09^2 = 0,0981

=> Corr (a,b) = covar (a,b) / var (a) * var (b) = 0,036 / sqrt(0,034 * 0,0981) = 0,62

Getting 0.625087 so B. Had to crack my notes open for the formula though so I guess I need to invest more time on those.