Vance Harwood has good stuff.

Yes, that is what I meant. Shorting SVXY is analogous to being long VXY correct? I am (clearly) not too versed on these vol tickers.

There’s a vol mega thread below. For a couple years I explored every instrument and strategy out there. In the end I came back to VIX futures if a short-term trade (trades around the clock so I can short during Asian market hours), or a VXX short for the longer-term decay game.

Basically I just short with a small initial bet anytime VIX spikes, and then martingale (double down) if it continues upward, with a final bet at VIX=60. But knowing that I’m going to do that, I also sometimes sell VXX calls to get paid to initiate the shorts at various upward levels, then get the short and ride the decay down, then sell a put to get paid to release the short… get paid three times.

It’s all about selling to optimists and buying from pessimists (although that is reversed with vol). If vol spikes but I don’t believe the hype then I’m going to short it and sell some expensive calls, if it chills and I don’t believe it’s over I’m going to sell puts to exit.

So the other day I took the CBOE PutWrite’s monthly excess returns since January 1990 through March 2017 and regressed them against the S&P 500 TR’s excess returns over the same time period. The p-value for the positive intercept term was 0.007… i.e., at any confidence level below 99.3% we can reject the null hypothesis that the intercept term is equal to zero. What’s there to be said about this?

Supposing that the equity risk premium was the only additional risk premium present in listed option contracts, the expected return on a portfolio that owns an underlying and maintains perfect delta-hedging put option positions at all times should not be different from zero. However I feel like I’ve seen and skimmed through several research papers that showed that this delta-hedged portfolio consistently posted negative returns, implying if I understood correctly that there seems to be a persistent negative risk premium that option buyers are paying in exchange for protection from additional skew and convexity in their portfolio. Is this non-zero risk premium then the cost associated with mitigating skew and convexity in a portfolio?

are one of you guys 50 cent?

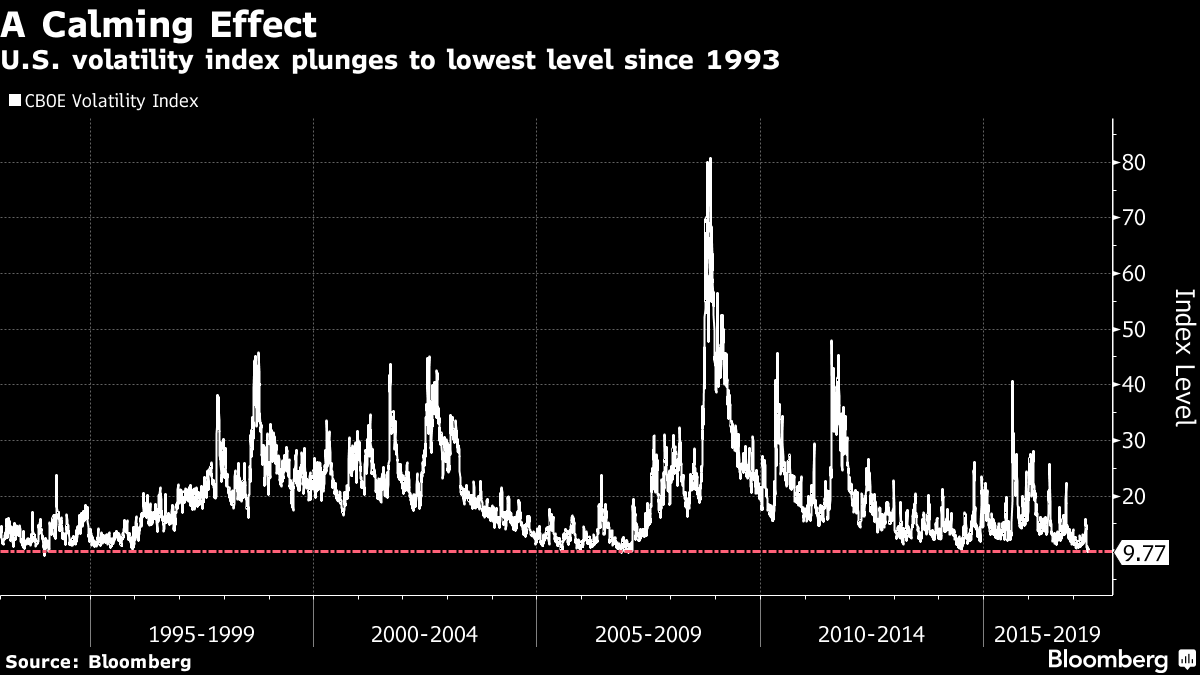

Speaking of VIX, lowest level since 1993.

I looked again at going long futures, but never done it and probably never will. The 50% decay / year or whatever is just too deadly. You get long, and if you don’t get a spike within a month you just end up dying a slow death, when do you make the call to take the loss? Long vol just creeps me out.

Also I looked at buying calls, but the prices totally suck.

Believe lowest VIX record was 9.39 in December 2006?

I’ll put about 5% on initial, then if it slips, double the shares I own, and if it’s slips again and I still think I’m right, either increase by the same amount or double again, depending on conviction.

At the time it always feels like a lot but the fresh capital from the human capital side of the portfolio will usually reduce the positions weight with time, unless the position goes up big league.

I hold until there’s is a better use for the capital, after considering taxes. Usually a very long holding period, ideally hold forever if it’s a good business.

3% - 15%, Hold for one year and then reevaluate (may continue to hold).

i think in like iras/roth iras. i would trade more often. like if it makes big stock moves, i will buy or sell.

but for taxable accts. i would prolly do jbrowntown strat. evaluate every 10-k release kind of thing. look at the after tax returns after selling then reinvesting. etc.

Man, you guys are all crazy. I just allocate between 3-5 low cost etfs. I never allocate more than 2% of my portfolio to an individual stock.

BTFD

There will be a time when vol is higher than the historical and these easy peasy strategy’s result in massive losses.

Nope, only if you sell. Already happened to me in 2015, losses = $0.

pa whats the word on ASHr

^ Not much happening, CSI300 grinding away from 3000 to 3400 over the last 12 months. CN must be liking the US meltdown, they’ll continue taking their place as the masters of the new universe. I see the greatest risk to ASHR just being the end of this bull market. Personally I’m gonna hold for life, but I’ve got cash ready to buy more when the bear comes.

are you ready for June?

^ Summer is when I get my phat dividends from ICBC, SAIC, etc, ready!

also when MSCI decides whether or not to add ASHR

^ Oh that again. Yeah, they have to add Chinese stocks eventually, but I gave up waiting. Big political scam.

huh? You’re short vol and you only lose when you sell?

Pics of account P&L or calling BS. You’re just a gambler with some serious hindsight and confirmation biases.