Consider a share of XYZ stock, with a current price of 50. Which of the following options portfolios on XYZ stock will most likely have the lowest vega? a. A long put with the strike of 10. b. A long call with the strike of 50 and a short call with the strike of 50. c. A long call with the strike of 90 Explain why.

B says you’re long and short the same call? i.e. flat? i’d think that would have the lowest volatility since more or less you are just boxed on the postion. who boxes options? this question is weird to me.

Sorry, a typo. Here it is 100% corrected. Consider a share of XYZ stock, with a current price of 50. Which of the following options portfolios on XYZ stock will most likely have the lowest vega? a. A long put with the strike of 10. b. A long put with the strike of 50 and a short call with the strike of 50. c. A long call with the strike of 90 Explain why.

i still like B- stock goes up, you get called out, stock goes down, you exercise your put. you’re pretty locked into $50, that seems like low vol to me even though A is way in the money and C is way out. am i right? out of the other 2- which of those would have a higher vega, the out of the money call or the way OUT the money put ? i’d want to guess maybe the call but i could be wrong. edit- the put is way OUT of the money not in. it’s been a long day. in that case… hmm… they’re both $40 bucks out of the money.

Vega(option) = Delta(option)/Delta(std deviation of underlying security).

The vega of a sum is just the sum of the vegas. Therefore, the long (positive vega) for the put should near cancel the short (negative vega) for the call in part B, and the portfolio should be vega neutral. For what it is worth, vega of a < vega of c.

But if the two vegas nearly cancel out, as you say, which of the three choices has the lowest vega? Isn’t part a’s vega very close to zero?

B. Both A and C will have very low but non-zero vega. B will have zero vega because calls and puts have the same vega, so being long one and short the other one will cancel each out precisely.

> b. A long put with the strike of 50 and a short call with the strike of 50. If the stock drops to $40, the long put value will gain $10, but the short call will drop by a smaller amount, because the put is now deep in the money, while the call is slowly going into out of the money mode. This idicates that the vegas are not the same. That is, the percentage change in the long put price is much more than the percentage change in the short call price. Agreed?

No…this indicates that the deltas are not the same. Mathematically speaking, all else equal, vega for a put is equal to vega of a call. Portfolio in B should be vega neutral, and therefore have a vega of zero.

ok, I’ll have to just memorize that because the example I mentioned above clearly (at least to me) shows it isn’t so.

The example you gave represents a change in the price of an option with respect to a change in the price of the underlying…this is delta. Vega is a measurement of the change in the price of the option with respect to a change in the volatility parameter holding all other factors constant (including price of underlying). Therefore, your example is not an example of vega, and does not clearly show anything. Vega being equal for a call and put is a mathematical fact.

wyantjs = greeks machine! i will get back to derivs soon. started FI today, have that and then i’ll get me to the greeks in maybe a week or 2.

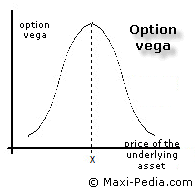

a picture says more than 1000 words…  http://www.maxi-pedia.com/web_files/images/Option_vega_greek.png

http://www.maxi-pedia.com/web_files/images/Option_vega_greek.png

{kind=link}

> Vega is a measurement of the change in the price of the option with respect to a change in > the volatility parameter holding all other factors constant (including price of underlying). “(including price of underlying)” is a keyword here which I was missing. Thanks for clarifying that, wyantjs. So, if the current price of the stock is $20 (and we still have one long put with $50 strike and one short call with also $50 strike), this then says that the percentage change in the put price due to an increase in volatility would be the same as the percentage change in the call price. If the put had a price of $30 before the change in volatility, and the call was at $0.05, then a sudden jump in volatility would result in the same percentage change in price for the two options? Hang in there, we’re almost there… so if the call price doubles in value to $0.10, the put price would decline by 50% to $15? I guess that is correct, I’ve seen that happen. Final question: Would this be the same if the portfoliio was one long put and one long call? Would the combined vega be zero?

No to both. The change is not a percentage change. It is an absolute change. Think about your example again. Why would a rise in volatility that increases the call price by $.10 also decrease a put by $15? Both would increase, and both would increase by the same dollar amount per option. As for the final question…The vega would simply be double the vega of the single option. Vega is always positive, but selling an option is equivalent to being short volatility, and hence the portfolio vega is reduced by the short position. If you are long both, then a sudden increase in volatility increases the value of both positions, thereby magnifying the increase in the value of the portfolio. So for the position in the original question, increases in volatility will increase the price of both the put and the call, but since you are long one and short the other, you will receive an equivalent gain on the long position as you will the loss on the put position. Result…no change in portfolio value.

for same strike price, same maturity, same underlying, same yield, same vola - both calls and puts have the same vega. theoretical numbers computed via MATLAB. ------------------------------ asset price=35 strike=50 annualized continuously rate=0.05 time=0.75 years annualized vola (asset)= 100% price of the options: [call, put] = (Price, Strike, Rate, Time, Volatility) [call,put] = (35, 50, 0.05, 0.75, 1) call = 8.2184 put = 21.3781 vega options: Vega=(35, 50, 0.05, 0.75, 1) Vega = 12.0672 --------------------------------------- now lets change the vola to 1.01 or 101% [newcall,newput] = (35, 50, 0.05, 0.75, 1.01) newcall = 8.3390 newput = 21.4987 *edit: as you can see the change in absolute terms is vega!!! ------------------------------------ again, ----> long call vega = long put vega = - short call vega = - short put vega as some pointed out earlier vega is additive. so to answer you final question: long means = +vega short means = -vega therefore answer b in your introductory question.

Thanks to both of you. wyantjs, you answered my question which I was just about to ask: why would +$0.10 in the call result in -$15 in the put? It is not percentage change but absolute change. Phew!