I’m not quite sure what you looked at, but the majority of borrowers are refinancing preexisting debt elsewhere. I think that’s roughly three quarters of LC loans.

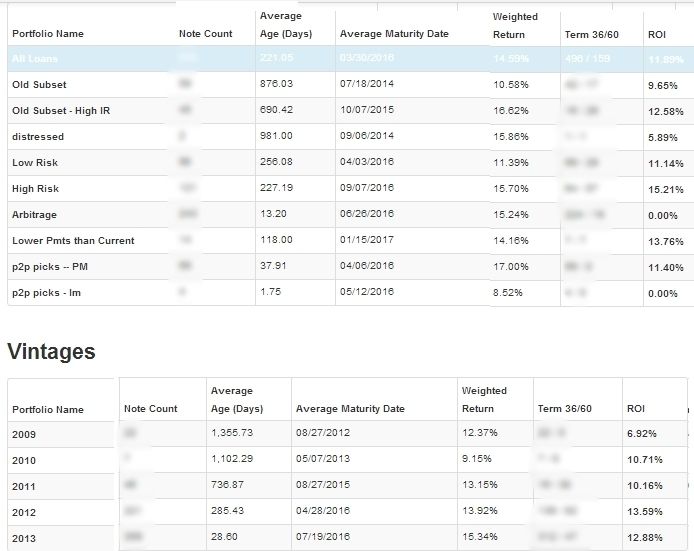

In terms of performance, this is my information by strategy and vintage.

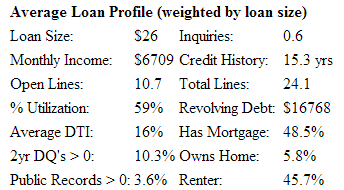

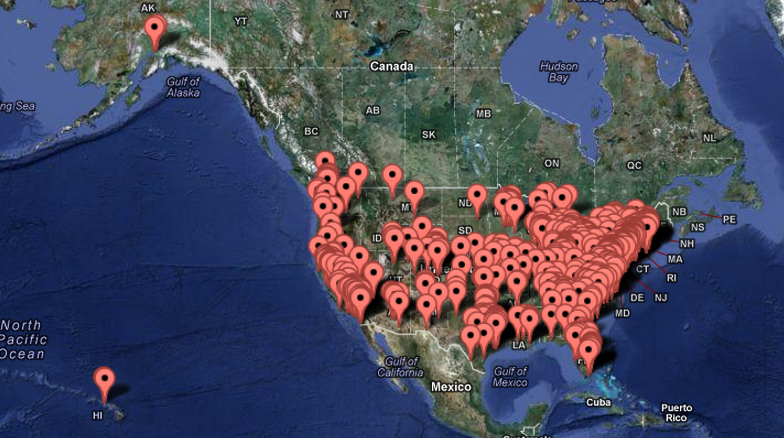

I started while in college and have geared up since I’ve graduated and have money to invest. That gives you some idea of the return and break down. Here are characteristics of my pool and geographic distribution:

So far it is treating me very well. I view it as securitizaton except I get to choose the characteristics of the investment. Pretty sweet deal IMO.

Average monthly Income is $6,700 and they need to turn to Lending Club? Or does LC buy the debt from banks and resell to joe schmo?

How do 48% have a mortgage but only 6% own a home? ANd if 45% rent that means the other 50% must live at home? But on average they’re making $80,000/year?

Smells like a rat, I’d like to buy some CDS’ on your portfolio. 8%-15% cost of capital isnt high enough for these scrubs.

You don’t own your home if you have a mortgage. If you don’t own your home or have a mortgage, you’re renting. Notice how those three numbers add up to 100%…

If you are a prime borrower, go around and price unsecured debt from a regular bank. THen compare to LC. LC will beat 9/10 times and its a function of reducing the “overhead” cost piece of the interest rate. And it’s easy, I can get a loan not leaving my bedroom.

I think the average FICO of the pool is something like 730. Definetly CDS worthy ^.-

I always find it funny people are very skeptical of things they aren’t familiar with. If people treated things they were familiar with in the same regard, we’d have a lot less boom/bust cycles.

Thanks for the data. It’s not unexpected that retail borrowers might be willing to pay higher interest rates for the same risk compared to institutional investors or companies. Plus, if they are anchored to absurd credit card rates, maybe they will view even high rates on Lending Club as a (misguidedly) good deal. This warrants further investigation…

LC has a range of probably 660 to 800+ Credit Scores. The 800+ people with low DTI, no recent inquiries, etc only pay like 6.03% interest (A1) to 20+ (G) loans. I’m primarily centered in ABC, although some go for a DEF strategy. I think that strategy will be much more susceptible to macro economic shocks. For example, with my FICO and financial info I qualify for a 9% ish loan, which isn’t terrible. And like you said, most of these are prime borrowers getting eaten alive by their APR on credit cards. So they turn revolving to installment and have a fixed maturity, often with the same or lower payment (due to lower rate).

If you want exposure to ‘lower’ credit quality, I’d check out Prosper. But I prefer investing higher on the FICO chain.

LC lists how they determine credit ratings. And the returns haven’t appeared to be correlate with stocks, bonds, etc (as LC started in the crisis during the credit freeze).

LC is currently exploring trying to do the same model for business loans. I don’t think I’d invest in that – that’s much more complex than consumer loans. LC also makes all data available, so there are some out there who have made some crazy econometric models to pick loans ‘mispriced’ by LC’s rate sheet.

I’ve done an analysis of LC data with the data set they provide. I will post it if I get a chance. My understanding is income from LC is taxed at your ordinary income tax level. It is not considered to be interest.

So when you look at after tax returns INCLUDING default rates the returns are not nearly as attractive as they seem.

That is correct about taxation, not sure what default rates you are using. It is also important to note that if you engage in the secondary market (such as selling notes), you have to itemize each transaction on one of those pesky forms. Can be a pain depending on your strategy.

The expected ROI of many of us who invest on LC using the historical data to inform future performance is probably 10-12% ROI pre-tax (NAR isn’t very useful). Given the lower violatility of that return, it works well to balance out my other more violatile investments. Lately instiutional money has flowed in. As a result, the loans are funding within minutes once posting.

This blog is sort of the “center” of the P2P universe. May want to check it out: http://www.lendacademy.com/ The most recent is about getting exposure to business loans. I’m not an accredited investor, so I haven’t considered it. But some of the BSDs here may be able to.